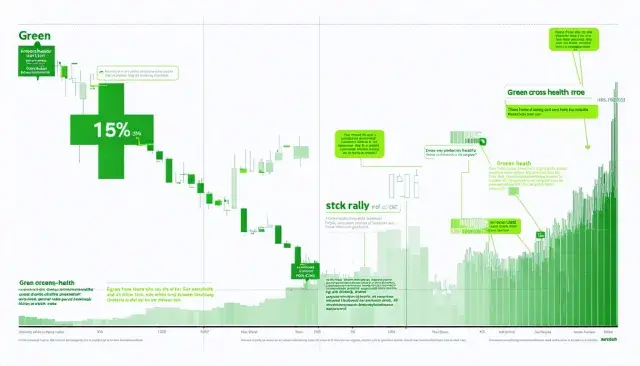

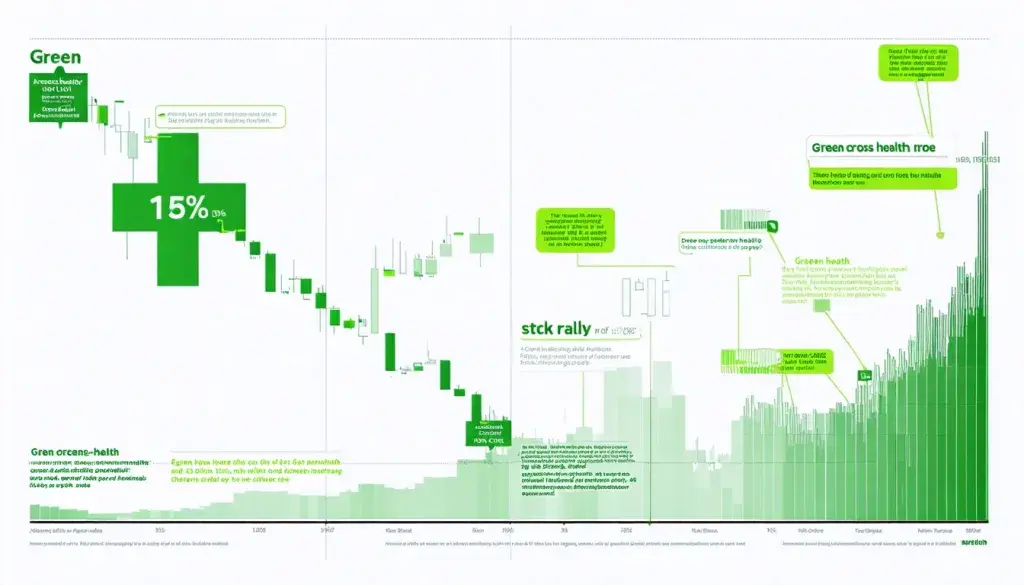

Green Cross Health (NZSE:GXH), New Zealand's leading pharmacy retailer, has seen its stock price rise a robust 15% over the past three months. This surge prompts investors to scrutinize underlying financials, particularly return on equity (ROE), to gauge if the rally reflects sustainable performance in a competitive healthcare landscape.

Decoding ROE: A Core Profitability Metric

ROE measures how effectively a company turns shareholder equity into profits, calculated as net profit from continuing operations divided by shareholders' equity. For Green Cross Health, this yields 12% based on trailing twelve months to September 2025: NZ$22 million net profit over NZ$180 million equity. This means every dollar of equity generates 12 cents in after-tax profit—a solid benchmark in retail healthcare.

- Formula: ROE = Net Profit ÷ Shareholders' Equity

- Green Cross Health's ROE: 12% (NZ$22m ÷ NZ$180m)

- Implication: Efficient capital use amid rising healthcare demands from an aging population.

ROE Matches Industry Norms Amid Earnings Dip

Green Cross Health's 12% ROE aligns precisely with the industry average, signaling competent management in a sector facing margin pressures from generics and online competition. Yet, net income fell 4.0% over the period, mirroring broader industry contraction. Factors like high dividend payouts—appealing to income-focused investors—or intensified rivalry may explain this, rather than operational flaws.

In New Zealand's pharmacy market, where community health services underpin public wellness, such stability underscores resilience. Stable ROE supports reinvestment for growth, even as earnings stagnate, tying into trends like expanded telehealth and preventive care.

Linking ROE to Growth and Valuation Insights

Higher ROE with retained earnings typically fuels expansion, but Green Cross Health's profile suggests dividend priority over aggressive growth. The 4% earnings decline, synced with industry trends, tempers optimism yet doesn't derail the stock's momentum—possibly driven by market bets on recovery via store optimizations or policy tailwinds.

- Industry earnings decline: 4.0% (same as company)

- Key drivers: Dividend focus, competition

- Broader context: NZ healthcare retail eyes 2-3% annual growth from demographics.

Outlook: Fairly Valued with Cautious Upside

With earnings growth baked into current pricing, Green Cross Health appears fairly valued relative to peers. Investors should watch for dividend sustainability and competitive edges in digital health integration. In a post-pandemic era prioritizing accessible pharmacy services, this 15% run highlights enduring appeal, but long-term gains hinge on reversing earnings softness.