Canopy Growth posted strong medical cannabis revenue growth for fiscal 2026, and the company made sure investors heard about it. That's standard earnings-season behavior. But cannabis industry observers - including operators, suppliers, and investors who track the Canadian licensed producer space - should read past the headline numbers before drawing any conclusions about where this company actually stands.

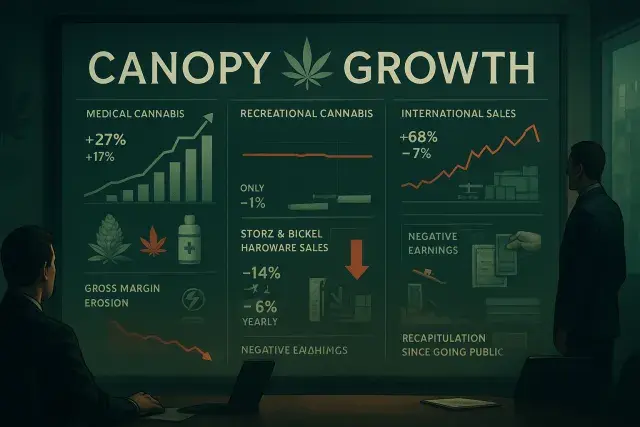

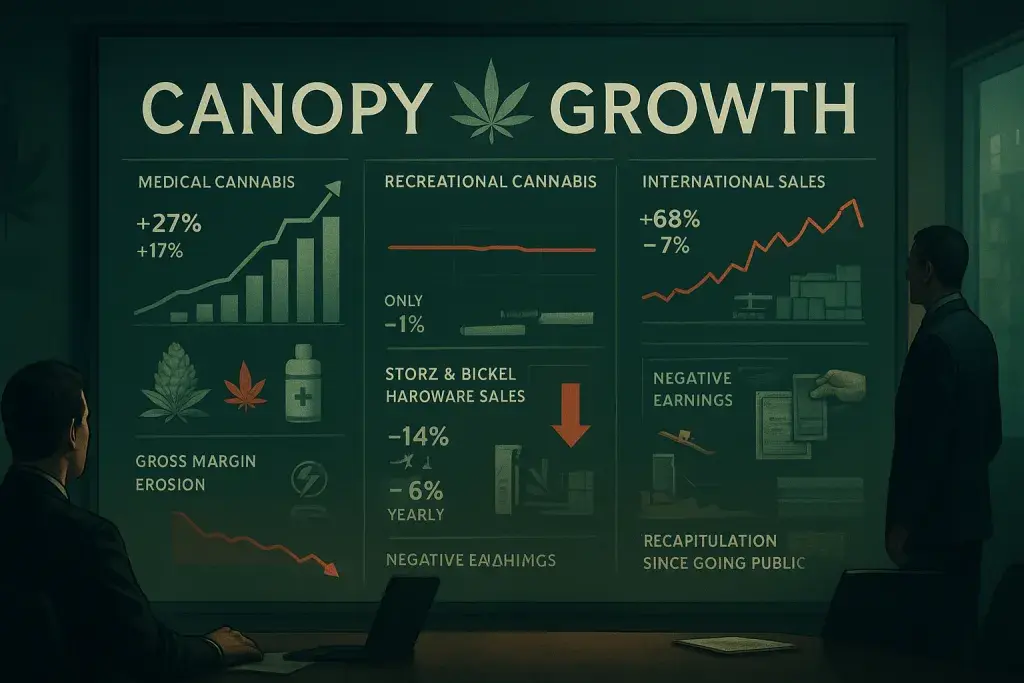

The medical marijuana division did perform well. Revenue grew 27% in the fourth quarter and 17% for the full fiscal year, and the recent acquisition of MTL Cannabis strengthens Canopy's position in the Canadian medical market further. Those are real results. But earnings reports from cannabis companies - like those from any publicly traded business - tend to lead with the strongest data, and any operator or investor who has built a cannabis retail platform for New York or another heavily regulated market knows the difference between a strong quarter in one channel and a healthy business across the board. A single well-performing division does not rewrite the broader story. cannabis retail platform for New York

Here's the catch. Canopy's recreational cannabis segment grew 20% for the full fiscal year - a figure that sounds solid - but recorded only 1% revenue growth in the fourth quarter. The company credited the full-year number to infused pre-roll offerings and new all-in-one vaporizer SKUs launched early in the year. That's a reasonable explanation, but a 1% finish to the year raises a fair question: did those product launches drive durable demand, or did they pull sales forward and exhaust early adopters? The fourth quarter's performance suggests the latter is at least worth considering.

Where the Mixed Picture Gets More Complicated

International cannabis sales swung sharply depending on how you measure them. Up 68% in the fourth quarter - striking on its face - but down 7% year over year. Supply chain disruptions were flagged as a contributing factor earlier in the fiscal year, which explains some of the quarterly volatility. Still, a business that finishes a full fiscal year with a net revenue decline in its international segment is not a business firing on all cylinders, regardless of what a single strong quarter suggests.

Then there's Storz & Bickel, Canopy's vaporizer hardware brand. Sales fell 14% for both the full year and the fourth quarter. That kind of parallel decline - consistent across both time frames - is harder to explain away as timing or supply disruption. It reads more like structural softness in demand, which matters because hardware has historically carried strong margins and served as a more stable revenue stream than flower or infused products.

Gross Margin Erosion Is the Number That Sticks

Revenue growth in one or two segments can obscure margin pressure, and that's exactly what happened here. Canopy's gross margin dropped four percentage points in the fourth quarter and six percentage points for the full fiscal year. In cannabis retail and licensed production, margin compression is a familiar and persistent problem - excise taxes in Canada are structured in ways that punish companies when wholesale prices fall, and input costs don't always move in sync with what operators can charge at the counter. But a six-point full-year margin decline is not noise. It's a signal that the cost structure is not keeping pace with revenue.

Negative earnings, again. Canopy Growth has not reported positive earnings since going public, and that spans more than a decade of operations. The company also recapitalized its balance sheet during fiscal 2026, exchanging shares for debt - a move that restructures near-term obligations but dilutes existing shareholders and changes the risk profile of the equity. For anyone evaluating this stock as a proxy for Canadian cannabis market health, that context matters.

What Operators and B2B Investors Should Take Away

The broader lesson here isn't specific to Canopy Growth. Earnings season across the cannabis industry consistently rewards careful readers. Licensed producers, multi-state operators, and cannabis retailers all face the same pressure to package their strongest metrics prominently - medical growth here, new market entry there, a flagship product launch front and center. That's not deception; it's standard investor relations practice. But the business fundamentals - margin trajectory, free cash flow, balance sheet structure, and performance across all segments - tell the more complete story.

For dispensary operators, wholesalers, and brands that track Canadian licensed producers as a window into where the broader North American market may head, the Canopy earnings report is a reminder that vertical integration and brand diversification don't automatically produce financial stability. A company can hold strong positions in medical cannabis, recreational, international, and hardware simultaneously and still lose ground on the metrics that determine long-term viability. One strong division keeps a story alive. It doesn't, by itself, justify a rally.